Switching Car Insurance Simplified Steps

Insurance

|

May 15, 2026

Switching car insurance might seem like a complex task, but with the right approach, it can be a simple process that not only saves you money but also enhances your coverage. Many drivers contemplate changing their insurance policies for various reasons, including the pursuit of better rates, more comprehensive coverage, or dissatisfaction with their current insurer. However, it’s crucial to manage this transition carefully to avoid potential coverage gaps that could leave you unprotected on the road.

Switching car insurance might seem like a complex task, but with the right approach, it can be a simple process that not only saves you money but also enhances your coverage. Many drivers contemplate changing their insurance policies for various reasons, including the pursuit of better rates, more comprehensive coverage, or dissatisfaction with their current insurer. However, it’s crucial to manage this transition carefully to avoid potential coverage gaps that could leave you unprotected on the road.

This guide will walk you through essential steps to ensure your switch is both smooth and efficient. From evaluating your current policy to researching potential new companies, we will cover everything necessary for making a well-informed decision. You will also learn about frequent mistakes to avoid and reasons when it might be beneficial to remain with your existing provider. Equipped with this knowledge, you can take charge of your car insurance needs and secure the best coverage tailored to your circumstances.

Why Drivers Switch Car Insurance Companies

Many drivers regard car insurance as a necessary yet often perplexing purchase. A variety of factors can motivate them to switch insurance companies, usually in pursuit of better value or enhanced service.

Rising Insurance Premiums

One significant factor prompting changes in providers is the rising insurance premiums. As costs climb due to inflation, shifting risk factors, or corporate policies, many drivers seek out more affordable alternatives. Conducting comparisons can unveil substantial savings, encouraging a switch.

Better Coverage Options

Drivers are also drawn to better coverage options. As individual needs evolve—for instance, needing additional rental coverage or roadside assistance—locating a policy that meets these new requirements can prompt a change. For example, a young driver may find a favorable plan that includes collision coverage tailored to their lifestyle.

Moving to a New State

An out-of-state move significantly affects insurance rates and regulations. Each state has distinct laws regarding coverage minimums and local risks, radically altering a driver’s financial obligations and the fairness of their policy.

Buying a New Vehicle

When acquiring a new vehicle, there's often a compelling need to reassess insurance needs, as rates can fluctuate based on a car's make and model. A higher-value vehicle usually necessitates more comprehensive coverage, prompting drivers to explore better-suited policies.

Marriage, Family Changes, or Retirement

Life transitions such as marriage, changes in family status, or retirement require policy evaluations. These moments lead to changes in driving needs and risks, making it vital for drivers to adapt their insurance accordingly.

Poor Customer Service or Claims Experience

Lastly, lackluster customer service or a negative claims experience can lead drivers to seek out a new provider. Difficult experiences during a claim can motivate individuals to find providers renowned for improved support and expedited processing times.

Collectively, these factors highlight the importance of regularly evaluating your car insurance to ensure it aligns with your current condition and requirements.

Can You Switch Car Insurance at Any Time?

Yes, drivers generally have the flexibility to switch car insurance at almost any time during their policy period. However, several factors must be taken into account before proceeding with the change. Primarily, it's vital to verify if your existing policy has cancellation fees, as some insurers impose these charges if you terminate your coverage early. For example, canceling your insurance a month before the renewal date might incur a fee that negates any savings achieved by switching to a new provider.

Additionally, state regulations concerning insurance cancellations can vary. Certain states might mandate insurers to provide specific cancellation notice periods, while others could have no restrictions. It’s crucial for drivers to familiarize themselves with their state’s rules to avoid any complications.

Though changing insurers tends to be straightforward, maintaining continuous coverage during the transition is crucial. Most drivers find that with adequate planning and comprehension of the process, switching insurance can be executed seamlessly and without much hassle, ultimately leading to improved rates and coverage fitting their needs better.

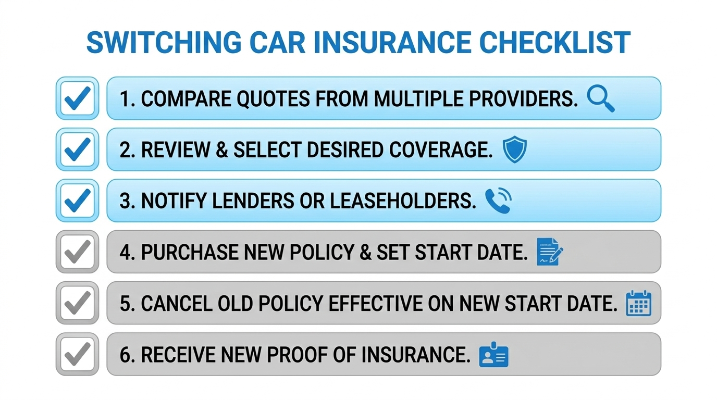

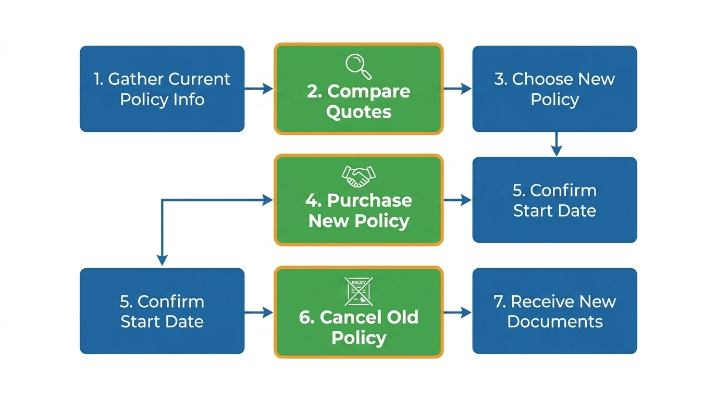

How to Switch Car Insurance in 7 Simple Steps

Although switching car insurance may seem intimidating, it can be accomplished smoothly by following these seven simple steps, ensuring no lapse in coverage.

Step 1: Compare Multiple Car Insurance Quotes

Engaging in comparisons of various car insurance quotes before making any decisions is essential. Utilizing websites and apps can help garner quotes from numerous insurers in a matter of minutes. While the premium amounts are critical, verifying that coverage levels align with your needs—typically including liability, comprehensive, collision, and personal injury protection—is equally important. Comparing quotes enables a clear understanding of the market and aids in securing better rates or coverage.

Step 2: Review Your Current Coverage

Take the necessary time to fully understand your existing policy. Assess your coverage limits, deductibles, and any available discounts. Familiarity with these details will assist in determining whether your new policy meets your insurance needs adequately. If uncertainty arises, enlisting an insurance agent’s help may provide clarity regarding terms and effective options for your situation.

Step 3: Purchase a New Policy Before Canceling the Old One

To prevent any coverage gaps, it is essential to buy the new insurance policy prior to canceling the existing one. Ensuring that the new policy begins the moment the old one concludes is vital in protecting yourself from becoming uninsured, which can bring severe legal and financial repercussions.

Step 4: Choose the Correct Insurance Effective Date

Align the effective date of your new policy with that of your current coverage expiration. If your old policy renews on a specific date, ensure your new policy begins on that date. When in doubt, reach out to your new provider for clarification on any overlapping or conflicting dates.

Step 5: Cancel Your Existing Policy Properly

After securing your new policy, it’s necessary to officially cancel your old one. Review the cancellation protocol of your current provider—some might require written notices, while others may allow cancellations via phone or online. Be mindful of any potential cancellation fees that may apply. Retaining a record of your cancellation is also highly advisable.

Step 6: Notify Your Lender or Leasing Company

If you are financing or leasing your vehicle, promptly inform your lender about the change in insurance. Providing proof of your new policy ensures that they maintain the appropriate records. Lenders generally want to confirm that their asset is continually covered, and notifying them can prevent complications in the future.

Step 7: Update and Store Your Proof of Insurance

Lastly, after activating your new policy, it’s crucial to obtain updated proof of insurance. Typically, this can be downloaded from your provider’s website or mobile app. Keep a copy in your vehicle and store a backup securely, such as in your smartphone or cloud storage. Proof of insurance serves as a necessary legal document and may be needed for lenders when applicable.

By following these seven steps, you can confidently switch your car insurance without risking coverage lapses or incurring unexpected charges. Regularly assessing your insurance options constitutes a savvy financial tactic, ensuring continued receipt of optimal coverage for your situation.

Common Mistakes to Avoid When Switching Car Insurance

Switching car insurance can often lead to better rates and more suitable coverage; however, several common pitfalls can hinder this otherwise straightforward process. Here are five critical mistakes to avoid:

- Canceling Coverage Too Early: One of the most pressing risks is canceling your existing insurance policy before activating a new one. This can leave you temporarily uninsured, exposing you to hefty fines or substantial financial liabilities if an accident occurs during this gap in coverage. Always ensure your new policy is active before discontinuing your old one.

- Comparing Policies Based Only on Price: Saving money is essential; however, focusing purely on price can be misleading. Different providers offer varying coverage levels and deductibles, so assessing the actual quality and details of each policy is critical to avoid sacrificing important protections like liability or collision coverage for a cheaper premium.

- Overlooking Coverage Differences: It’s crucial to scrutinize the fine print in any policy. Coverage limits can differ dramatically across insurers, and choosing an inadequate policy will leave you underinsured, resulting in potentially high out-of-pocket costs in the event of an accident. Ensure the fundamental aspects of your coverage adequately address your needs before proceeding with a switch.

- Forgetting About Lender Requirements: If you finance your vehicle, your lender likely has specific coverage levels they require. Failing to communicate with your lender about your insurance switch could unintentionally breach your loan agreement, resulting in financial penalties or forced insurance purchases at inflated rates.

- Ignoring Cancellation Terms and Fees: Each policy may impose cancellation fees or require advance notice before termination. Not understanding these terms can lead to unexpected expenses. Familiarize yourself with your existing policy’s cancellation process to sidestep any surprises.

Avoiding these common errors can facilitate a smoother transition between insurance policies and help protect you on the road.

How Often Should You Compare Car Insurance Quotes?

To capitalize on the best car insurance deals, routinely evaluating your options is essential. Drivers should conduct an annual review of their insurance policies. This consistent check enables comparisons across various providers and helps determine if your current policy remains aligned with your needs.

In addition to yearly evaluations, significant life changes should prompt reassessments of your coverage. For instance, purchasing a new vehicle or changing residences can significantly impact your rates and coverage requirements. Major life milestones like marriage or transitioning in employment status may also offer discounts or necessitate policy revisions.

To proactively manage your insurance needs, schedule a calendar reminder for annual assessments and create a checklist of factors that might necessitate a re-evaluation. Monitor evolving circumstances and gather quotes from a minimum of three providers to make sure you’re making informed decisions surrounding your coverage. By being proactive, you can sidestep overpaying for insurance and ensure adequate protection on the road.

Was this helpful? Share your thoughts